{kind=link}

{kind=link}

Sign up for notification of major updates and related work.

Consumer Protection in Online Discount Voucher Sales We evaluate five areas where online discount voucher services -- Groupon and similar sites -- risk falling afoul of applicable consumer protection law. We present applicable laws from selected states and evaluate compliance by voucher services and their affiliated merchants. We examine voucher services' attempts to limit their liability, and we explain why consumers and regulators should find current practices insufficient. |

Related Projects Voucher Complaints - Letter-Writing Tool Deception in Post-Transaction Marketing False and Deceptive Pay-Per-Click Ads |

Groupon's recent S-1 sparked renewed discussion of the viability of discount vouchers. David Sinsky and Felix Salmon ponder Groupons profitability, while Stat Spotting and my December 2010 paper (with Sonia Jaffe and Scott Kominers) evaluate discount offers from a merchants perspective. The results are potentially worrisome for voucher providers: If existing customers begin to buy discount vouchers, retailers cannot easily recruit enough new customers to make up the loss from discounting existing customers.

Voucher services operate in a highly regulated space -- discounting food and alcohol, while requiring prepayment and serving as intermediaries between myriad consumers and merchants. With such complexity in such highly regulated fields, voucher services naturally face numerous consumer protection laws restrictions which complicate certain marketing practices and may disallow others altogether.

Eric Lefkofsky, the largest shareholder in Groupon, says Groupon cant worry about the noise that the legal system creates. But in the following sections we present a series of consumer protection and regulatory concerns that extend beyond noise to raise serious questions about both the lawfulness and the sustainability of current discount voucher practices.

Taken individually, each problem might be resolvable. But in combination, these problems reveal the striking complexity and substantial legal exposure endemic to the business model voucher sites have chosen.

Restrictions on Discounts on Alcoholic Beverages

Voucher discounts on alcoholic beverages were in the news in March 2011 when Groupon reported that the Massachusetts Alcoholic Beverages Control Commission indicated Groupons offers did not comply with Massachusetts liquor laws which restrict discounts on alcoholic beverages. In an email to consumers who had purchased Groupon vouchers purportedly covering alcohol in Massachusetts restaurants, Groupon said it only "recently received notification" (emphasis added) of the Massachusetts law at issue -- suggesting that the Massachusetts law came as a surprise to Groupon. But the Alcoholic Beverages Control Commissions letter to Groupon characterized Massachusetts law as setting "long-established, clear, bright lines" -- indicating that Groupon should have complied with the law all along. Indeed, the text of Massachusetts §204-4.03(1)(c) plainly prohibits "sell[ing], offer[ing] to sell or deliver to any person ... any drinks at a price less than the price regularly charged for such drinks during the same calendar week." Furthermore, §204-4.03 specifically covers both "licensees" (those licensed to sell alcoholic beverages) as well as the "employee[s] or agent[s] of a licensee", a category which squarely covers marketing agents such as Groupon. We see no interpretation of the applicable Massachusetts law that would permit discount voucher sales of alcohol.

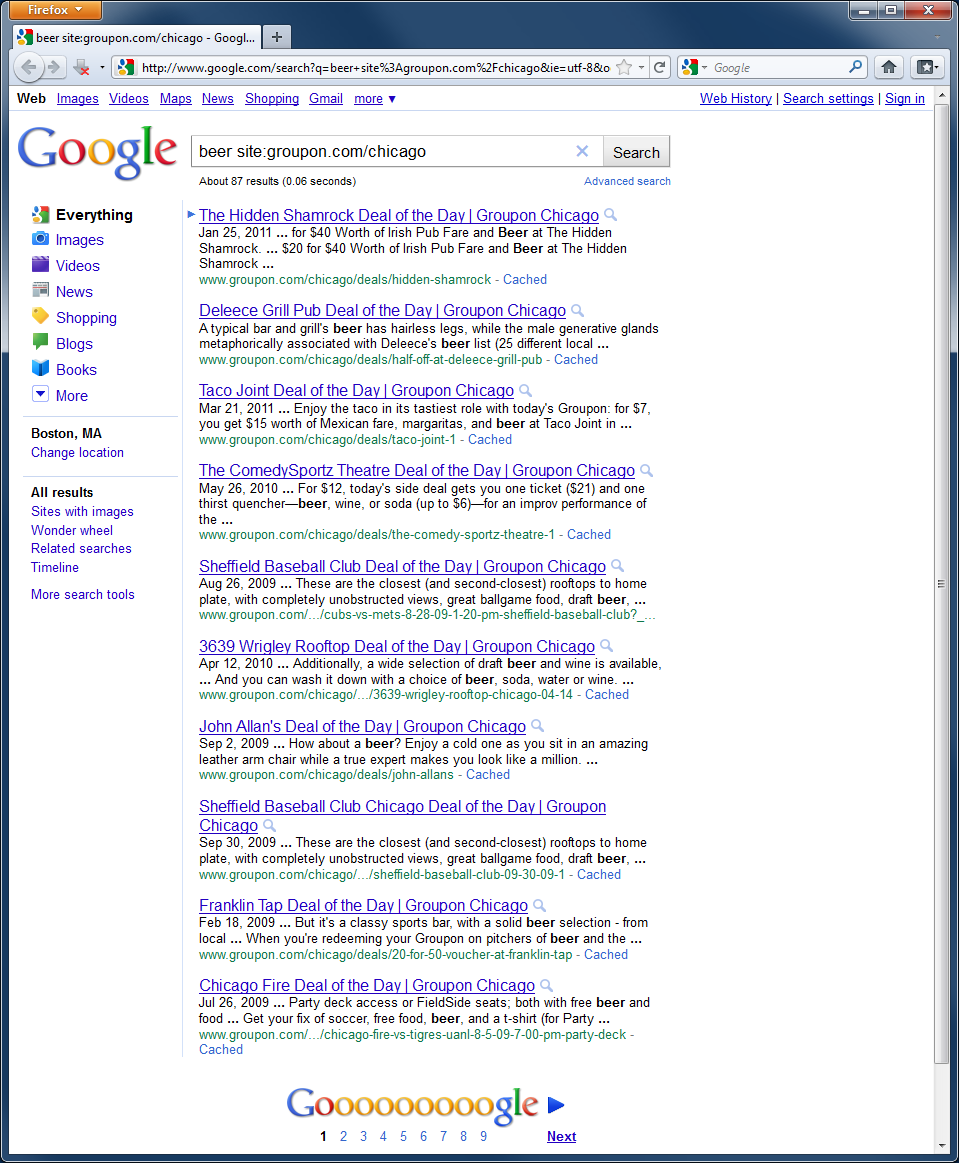

Various blogs and discussion forums suggested that Massachusetts alcohol rules are unusual in disallowing discounted alcohol sales. We disagree. For example, Groupons home state, Illinois, also restricts discounts on alcohol. In particular, §235 ILCS 5/6-28(b)(3) provides that no licensee (or agent) may "sell, offer to sell or serve any drink of alcoholic liquor to any person on any one date at a reduced price other than that charged other purchasers of drinks on that day where such reduced price is a promotion to encourage consumption of alcoholic liquor." Any voucher valid towards alcohol clearly results in sales at prices lower than those charged to customers without vouchers. Surely discounts on alcohol do encourage consumption, particularly when marketing pitches specifically feature redemption towards alcohol. Using Google, we readily found 87 Groupon vouchers in Chicago that mention "beer" in their descriptions and 252 that mention wine -- exactly the encouragement that the Illinois statute prohibits. Meanwhile, one Groupon offer promised $20 for $30 of alcohol at a Chicago market an offer "valid only for alcohol", not usable on any non-alcoholic items. We see no way to reconcile this promotion with applicable Illinois law.

Similarly, the Texas Alcoholic Beverage Commission disallows "any rebate or coupon redeemable for the purchase of any alcoholic beverage." Yet here too, Groupon has scores of discounts on alcohol.

While California does not restrict discounts on alcoholic beverages, the California Department of Alcoholic Beverage Control in 2009 issued an advisory noting that "management decisions, pricing decisions, controlling the distribution of funds, and profiting from the sale of alcoholic beverages are considered fundamental privileges of a licensee" and may not be performed by non-licensees. Thus, a discount voucher service may violate California ABC rules by profiting from the sale of alcohol. The California ABC allows "nominal transaction fees charged by independent financial service providers" when such fees are "de minimis and otherwise unrelated to the sale or promotion of the product." On one hand, discount voucher service fees are in some respects unrelated to the sale of alcohol: a voucher vendor collects the same fee whether a consumer purchases all alcohol, all food, or some combination thereof. On the other hand, prevailing fees are more than "de minimis"; Groupon typically charges 50%, a far cry from the 2%-4% credit card processors collect. And as in Chicago, hundreds of California Groupon offers specifically tout the use of vouchers towards beer, wine, or other alcoholic drinks. (Los Angeles: 30 beer, 123 wine; San Francisco: 9 beer, 86 wine.) With large fees from promoting alcohol purchases, voucher services probably fall afoul of California's 2009 advisory on non-licensees.

Nor are Massachusetts, Texas, and California alone in imposing such rules. The Texas Alcoholic Beverage Commission offers a map and table analyzing state "happy hour" laws, flagging 27 states with restrictions on drink discounts.

Groupon's approach in Massachusetts was to sell discount vouchers valid for alcohol until the Massachusetts ABCC specifically told Groupon it must not do so. But is that enough? Applicable Massachusetts law covers both sellers of alcoholic beverage and their marketing agents, and applicable California law flags sales activities that may not be performed by non-licensees. These laws apply to discount voucher vendors whether or not a voucher vendor is specifically notified by an applicable regulator. It seems to us that discount voucher vendors err in offering vouchers valid towards alcohol in the 27 states that limit or disallow discounts on alcohol. If voucher vendors ignore the law pending regulators' complaints, they should anticipate that regulators will in due course seek not just cessation of that impermissible activity going forward, but also disgorgement and penalties for the period of violation.

Prohibition on Short Voucher Expiration

Most current discount vouchers include text, often on the face of the voucher, listing an expiration date. Typically, the amount of the discount expires after three to six months, while most discount vouchers now provide that a customers prepayment remains valid for at least a year and often longer. These provisions at least assure that consumers will not soon lose the value they actually paid. But is this sufficient under prevailing consumer protection regulations?

The National Conference of State Legislators reports restrictions on the timing of gift certificate expiration in 27 states, while the federal Credit Card Accountability Responsibility and Disclosure Act (CARD Act) requires a minimum 5-year expiration nationwide. Importantly, where these laws apply, they typically cover the entire face value of a gift certificate, even if a user managed to purchase the gift certificate for a price less than the certificate's face value. For example, Illinois 815 §505/2SS(a)) defines a gift certificate to include any "record evidencing a promise, made for consideration ... that goods or services will be provided" a definition that easily includes Groupon-style discount vouchers. That definition leaves open the possibility that the "consideration" a consumer pays may be less than the face value associated with the gift certificate, but nothing in the statute indicates that the prohibition on short expiration would be limited to the amount of the consumer's prepayment. To the contrary, 2SS(b) exactly requires that the full amount of the gift certificate remain available for at least five years.

Similarly, in Massachusetts, a "gift certificate" is defined as "a writing [in] any medium that evidences the giving of consideration in exchange for the right to redeem the medium for goods, food, services, credit or money of at least an equal value." (MGL §255D.1) Notice the statute's mention of redemption "at least ... equal" to purchase price -- contemplating gift certificates redeemable for more than their purchase price. As a result, in Massachusetts, a prepurchased discount voucher must last for the seven years provided by Massachusetts law (MGL §266.75C), and the entirety of the value -- not just the consumer's purchase price -- must remain available for that period.

California is in accord. California's ban on gift certification expiration dates (§1749.5(a)(1)) includes an exception for gift certificates provided under a "promotional program without any money or other thing of value being given in exchange for the gift certificate by the consumer" (§1749.5(d)(1)) (emphasis added). But Groupon-style vouchers are sold to consumers for a fee, rendering the "without any money" exception inapplicable. Furthermore, California's §1749.51 instructs that a consumer may not waive these benefits, so even if a discount voucher service asked a consumer to accept an expiration date, any such agreement would be ineffective.

Connecticut's consumer protections in this respect are particularly noteworthy. Connecticut defines a gift certificate to be " a record evidencing a promise, made for consideration, by the seller or issuer of the record that goods or services will be provided to the owner of the record to the value shown in the record" (Conn. Gen. Stat. §3-56a(5)). Connecticut categorically disallows the sale of gift certificates with expiration dates: "No person may sell or issue a gift certificate, as defined in section 3-56a, that is subject to an expiration date" (Conn Gen. Stat. §42-460(a)). Notably, Connecticut also bans statements claiming that gift certificate value expires: "No gift certificate or any agreement with respect to such gift certificate may contain language suggesting that an expiration date may apply to the gift certificate" (Conn Gen. Stat. §42-460(a)) (emphasis added). Groupons vouchers fail Connecticuts ban on "language suggesting" expiration: Groupon includes an expiration date on every PDF voucher, and Groupon erroneously claims that the promotional value expires.

Analysis under the Federal CARD Act is a notch more complicated. At 15 USC §1693l-1(a)(2)(B), the CARD Act defines a "gift certificate" as

an electronic promise that is

(i) redeemable at a single merchant or an affiliated group of merchants that share the same name, mark, or logo;

(ii) issued in a specified amount that may not be increased or reloaded;

(iii) purchased on a prepaid basis in exchange for payment; and

(iv) honored upon presentation by such single merchant or affiliated group of merchants for goods or services."

A standard Groupon-style discount voucher satisfies each of these conditions. A subsequent exception, (D)(iii), excludes "promotional gift card[s], as defined by the [Federal Reserve] Board." Is a Groupon-style discount a "promotion" within the meaning of this exception? FRB e-CFR Title 12, §205.20(a)(4) indicates that any such discount must be issued pursuant to a "promotional program." On one hand, voucher services do require consumers to create accounts -- arguably joining a discount "program." Yet the offers are made available to the general public, and the "program" rules are just the sum of the rules of the individual offers, making the "program" look vacuous. The official staff interpretation of §205.20(a)(4) confirms that "coupons or discounts redeemable for or towards goods or services" can constitute a "promotional program" a requirement that Groupon-style discount vouchers can probably satisfy. But the staff interpretation is silent on whether promotional cards purchased for consideration would still fall within the "coupons or discounts" the staff propose to exclude from CARD Act expiration rules; since coupons and discounts are more commonly provided to consumers without an up-front charge, we see a strong interpretation that Groupon-style prepurchased vouchers do not fit within this exclusion.

In any event, the CARD Act's §205.20(a)(4)(iii)(A) limits promotional voucher exclusions to promotional vouchers which include "a statement indicating that the [offer] is issued for loyalty, award, or promotional purposes." We have seen no such statement on the discount vouchers that we have examined (from Groupon or others). For lack of the required statement, the "promotional program" exception probably does not apply and the CARD Act's protections remain. In particular, CARD Act §1639l-1(c) disallows any expiration in less than five years -- and just as in the states detailed above, this prohibition applies to the full value, including the amount of the discount.

Despite these state and federal regulation requiring extended validity of the full amount of a voucher, Groupon advises merchants that they need honor only the amount of a consumer's prepayment. For example, Groupon told the Consumerist that after expiration, "the merchant will still have to honor what you PAID (NOT face value)" (emphasis in the original). Tiny print at the bottom of each Groupon printout offers a similar statement. We've noticed similar practices at Livingsocial, BuyWithMe, and myriad similar sites. Groupon calls its approach the "more stringent" interpretation of applicable law, but we can't agree; to the contrary, applicable law seems to require more -- honoring the full face value, not just the customer's prepayment.

For Groupon and merchants, an extended validity reduces one source of profit anticipated by Groupon's current pricing model. As Stat Spotting points out, the nonredemption of discount vouchers offers a potential benefit to merchants participating in Groupon, for merchants can retain consumers' prepayment but need not provide much or any service. Outside the United States, the benefit of unredeemed vouchers currently flows to Groupon: Groupon's S-1 (p.15) says that Groupon pays most non-US merchants only when a consumer redeems a voucher. If vouchers have a longer validity period than Groupon and merchants anticipated, redemptions will increase -- to consumers' benefit but with a corresponding reduction in windfall profit to Groupon and merchants.

At least twelve lawsuits have already challenged Groupon's expiration practices: Arliss v. Groupon (Washington), Bates (Massachusetts), Booth (Illinois), Christensen (Minnesota), Cohen (Florida), Eidenmuller (California), Ferreira (California), Gosling (California), Johnson (Illinois), Meleh (California), Vazquez (District of Columbia), and Zard (Minnesota). These cases were recently consolidated in the Southern District of California, but to date there have been no substantive rulings in any of the cases.

Restrictions on Disposition of Abandoned Property

If a consumer fails to redeem a discount voucher, many states treat the amount of the non-redemption as unclaimed property subject to escheat to the state. For example, Illinois law provides that gift certificates and gift cards are among the types of property subject to transfer to the state upon expiration (765 ILCS 1025/10.6). As detailed above, discount vouchers fall within the definition of gift certificates in Illinois, and are therefore subject to Illinois requirements for unclaimed property.

So too in New York, where the Miscellaneous Unclaimed Property statute (§1315) requires that unclaimed gift certificates be remitted to the state after five years.

A historic Groupon merchant agreement reveals Groupon specifically requiring merchants to comply with any applicable laws as to unclaimed property. Groupon's current Merchant Terms and Conditions contain no such provision but do require merchants to "comply with all Laws" (6.1). Is that sufficient to absolve Groupon of liability when merchants predictably fail to remit funds to the state? We have our doubts, as we discuss below.

A Consumer's Right to Cash Back

In many states, a consumer prepayment (by gift certificate or similar) offers a right to a cash refund after a consumer redeems a specified portion of the prepaid value.

For example, in California, §1749.5(b) provides that a gift certificate with less than $10 of cash value remaining may be redeemed for cash. Because this provision applies to "cash value," the best interpretation is that a customer may receive cash back only from the amount the consumer paid, not from the amount of the discount. For example, if a consumer buys a $20-for-$40 Groupon and later seeks to spend just $12, this provision requires that the merchant provide the consumer with $8 in cash.

The National Conference of State Legislators reports that eight states require merchants to provide cash-back on a consumers request, including California (when remaining value declines to $10), Colorado (at $5), Maine ($5), Massachusetts (10%), Montana ($5), Rhode Island ($1), Vermont ($1), and Washington ($5).

In contrast, online discount vouchers often indicate that cash-back is not permitted. For example, Groupons "universal fine print" (present on all current Groupon vouchers) says "Not valid for cash back (unless required by law)." But applicable law in many states provides that consumers are in fact entitled to cash back in the circumstances detailed above. By suggesting otherwise, Groupon leads its consumers to mistakenly conclude they may not claim cash back. Nor does Groupons parenthetical offer consumers realistic assistance, for it is unrealistic to ask individual consumers to research what the law requires. Instead, we suggest Groupon should remove the "Not valid for cash back" statement from vouchers in states that allow cash back. Better yet, Groupon could adjust its vouchers to include a correct statement of applicable law in the corresponding state.

Sales Tax on the Amount of the Discount

When a consumer pays in part with a discount voucher, should sales tax be collected on the usual retail price of the consumers purchase, or on the amount the consumer actually paid? For example, if a consumer redeems a $20-for-$50 voucher on $50 of food, does the consumer pay sales tax on $20 or on $50?

Massachusetts has offered clear guidance on taxation of discount vouchers as applied to food. Massachusetts Department of Revenue Letter Ruling 84-74 states that a discount on food is non-taxable when a restaurant receives no reimbursement for the value of the coupon. Of course discount vouchers do yield a payment from the voucher vendor to the restaurant. Edelman therefore sent an inquiry to the Massachusetts Department of Revenue, Rulings & Regulations Bureau, which provided a prompt letter reply. That letter specifically confirms that an online discount voucher is "the equivalent of a cash discount by the restaurant" since the restaurant itself funds the totality of the discount. Thus, the letter indicates, Massachusetts sales tax should be calculated based on the amount the consumer actually pays, even if ordinary menu prices are higher.

Texas regulators reached the same conclusion. Forbess Janet Novack quotes a spokesperson for the Texas Comptroller affirming that Texas consumers should be charged tax only on what they actually paid. Indeed, Texas Administrative Code Title 34, Part 1, Chapter 3, Subchapter O, Rule 3.301(e) provides that "When coupons or certificates are accepted by retailers as a part of the selling price of any taxable item, the value of the coupon or certificate is excludable from the tax as a cash discount."

Janet Novack also reports California, Florida, and Illinois telling merchants to collect tax on the ordinary price of consumers purchase. But in all three cases, such an instruction is inconsistent with the corresponding state laws and regulations. For example, Illinois rules indicate that the amount of the discount should be nontaxable. Illinois Administrative Code 86 §130.2125(b)(2)(A) provides that "If a retailer allows a purchaser a discount from the selling price on the basis of a discount coupon for which the retailer will receive full or partial reimbursement (from a manufacturer, distributor or other source), the retailer incurs Retailers' Occupation Tax liability on the receipts received from the purchaser and the amount of any coupon reimbursement." Thus, an Illinois merchant should charge a consumer sales tax on the amount of its net receipt from the discount voucher vendor. For example, if the consumer bought a $20-for-$50 voucher and the voucher vendor remitted $10 to the merchant, then sales tax is payable on $10. At most a merchant might plausibly charge the consumer tax on $20 treating the consumer's payment to a voucher vendor, the merchant's agent, as payment to the merchant. But Illinois sales tax could not properly be charged on the $50 of menu price.

Florida law reaches the same result. Florida Administrative Code §12A-1.018 specifically provides that "discounts allowed and taken at the time of sale are deducted from the selling price, and the tax is due on the net amount paid." We do not see the rationale, under Florida law, for charging Florida tax on pre-discounted menu prices.

In California, §1671.1(b)(4) states that the value of a discount coupon is subtracted from an establishments gross receipts (and hence not subject to sales tax) when the consumer paid "no consideration" for the coupon. The cost of the coupon is, however counted in gross receipts when "the customer has previously given compensation to the retailer for the coupon." Groupon-style discount vouchers do not perfectly fit these categories: a consumer tenders prepayment to Groupon which deducts a fee and forwards the balance to the merchant -- compensation paid, at best, indirectly to the merchant; and no compensation offsetting the amount of the discount from face value. Meanwhile, the final sentence of §1671.1(b)(4) gives an example closer to Groupon-style vouchers: In the case of a coupon booklet sold by a retailer to a customer, the "pro rata share of the cost of the booklet represented by the purchase " is counted into gross receipts. Treating a Groupon as a single-coupon booklet, this example indicates that a consumer should be taxed on the amount paid for the Groupon voucher, but not on the amount of the discount the same result as in Massachusetts and Texas.

Following up on Edelman's 2010 letter to the Massachusetts Department of Revenue, we recently wrote to tax regulators in eight additional states. We have not yet received their replies. We will update this page if they offer views on correct taxation of discount vouchers.

In spring 2010, Edelman wrote to Groupon customer support to direct Groupon's attention to the Massachusetts rules and the letter referenced above. Groupon's Joe Harrow replied that "on the advice of our accountants, who looked into this issue for some time, we now typically advise the merchants we worked with to tax on the full promotional amount." Joe said this approach is preferable because it "has the least risk of increasing the business's liability." Groupon errs in advising merchants to overcollect tax to an extent beyond the amount actually required by law; merchants should collect exactly the correct amount of tax, not more or less.

In spring, Edelman also wrote to BuyWithMe, a discount voucher site which began in Boston. BuyWithMe's Tali replied to say BuyWithMe was "in the process of looking into this matter" but offered no substantive reply. Edelman sent multiple follow-up inquiries but received no reply.

As users of discount vouchers, we have found that most merchants charge tax on their full menu prices totaling all items ordered, multiplying by the tax rate, then deducting the face value of a discount voucher as a partial payment. This method is incorrect in light of the instructions provided by Massachusetts and Texas regulators, but we have failed in our efforts to alert Massachusetts merchants to the proper approach under applicable law.

Crude Redemption Processes Risking Errors and Abuse

We are struck by the crudeness of prevailing redemption processes. Many merchants simply write down a voucher number or cross of a line on a preprinted list of valid vouchers. These approaches invite errors both accidental and malevolent. For example, what if a merchant accidentally writes down or crosses off the wrong number -- transposing two numbers, or jumping to an adjacent line? Could a sophisticated attacker find a way to generate seemingly-valid voucher numbers? In either case, an affected consumer would find a voucher dishonored through no fault of the consumer. In our experience, such problems are awkward and difficult to resolve, especially because merchant staff seem to have received little or no training on consumers' rights or how to proceed.

In contrast, most other payment systems have established methods to check and reconcile transactions. Consumers' rights in credit card disputes are well-established through cardholder agreements, card network dispute processes, and federal law. Even stored value cards keep records of who bought what when. For many transactions, signatures provide a basic, if imperfect, method of verification. With modern IT and no constraints from legacy systems, discount vouchers have the potential to offer increased security and reliability, but instead current systems have been remarkably simplistic and ripe for abuse. At the very least, discount vouchers should clarify processes in case of error or other dispute.

Voucher Services' Liability for Merchant's Non-Performance and Other Infractions

Merchants can fall short of their obligations under a discount voucher in myriad ways. For example, a merchant might subject vouchers to undisclosed capacity constraints, disallow redemptions on "specials" (e.g. disallowing use towards prix fix menus, multi-course orders, brunches, or buffets, when voucher terms mentioned no such restrictions), require that consumers spend more than voucher terms specified, or impose a lengthy redemption process.

Anticipating these many possible disputes, voucher services typically seek to cast themselves as mere marketing vendors that are not responsible for the conduct of the corresponding merchants. For example, Groupons Terms of Sale claim that "The Merchant, not Groupon, is the seller of the Voucher and the goods and services and is solely responsible for redeeming any Voucher you purchase." On this view, a voucher service avoids liability for merchants' shortfalls.

But a voucher service is the merchant of record for the charge to the customer's credit card. As the entity officially responsible for charging the consumer, the voucher service thus faces increased responsibility to see that the consumer receives what was promised. Furthermore, the voucher service, not the merchant, writes the promotional text touting the merchants offering. As Rakesh Agrawal points out, Groupons financial disclosures even count the entirety of the consumers purchase price as revenue to Groupon. In this context, a consumer naturally looks to a voucher service for assistance if a merchant fails to perform. We think it is probably an unfair and deceptive practice, under the FTC Act and state equivalents, for voucher vendors to attempt to disclaim liability in such circumstances.

More generally, we are struck by Groupon's attempts to push all responsibility to merchants. On every relevant question -- discounting alcohol, honoring expiration dates, providing cashback -- Groupon's historic contract and current Merchant Terms of Service claim merchants are responsible. In our view, this approach invites confusion and non-compliance. Voucher services are far better positioned than merchants to determine what the legal system requires: Voucher services can research regulations centrally, once for each state in which they operate, then notify affiliated merchants of applicable requirements. In contrast, Groupon's current approach asks each individual merchant to conduct its own research. If merchants actually conducted such research, it would be duplicative and potentially wasteful -- thousands of small businesses re-researching the same questions. But in fact merchants typically ignore the questions, rationally concluding that these questions are too difficult for them to address on their own. Thus, by pushing merchants do to the work individually, voucher services virtually assure that the work is not done at all.

Importantly, the legal and regulatory questions flagged in this article are questions that arise distinctively in the context of discount vouchers: a merchant would never confront such questions were it not for discount vouchers. Having created the transactions giving rise to this regulatory complexity, we think discount voucher services should be expected to achieve compliance.

Finally, while voucher services attempt to push responsibility and liability to merchants, we see multiple areas in which voucher services are directly liable for their own activities, separate and apart from merchants' actions. As to alcohol discounting, we pointed out that Massachusetts and California law specifically restrict the activities of marketing agents. So too for expiration: For example, Massachusetts MGL §266.75C imposes liability on "whoever sells or offers to sell a gift certificate ... which imposes a time limit of less than 7 years" (emphasis added). Similarly, California §1749.5(a) provides that "It is unlawful for any person or entity to sell a gift certificate ... that contains ... an expiration date" (emphasis added). Voucher services do indeed "sell" the offers: voucher services present the terms, solicit purchases, and charge consumers' credit cards. Indeed, voucher services go further: They print "Expires on" dates on consumers' vouchers, they make statements about consumers' supposed legal rights as to voucher expiration, and they usually move "Expired" vouchers to a less prominent area of a user's online account. We see no way to reconcile these activities with applicable state law disallowing short expirations. Voucher services could therefore face direct liability for their actions in selling vouchers with short expiration dates and in labeling vouchers as expiring or expired.

The Public Policy of Applicable Restrictions

On one view, the legal requirements detailed above may seem burdensome. If restrictions are well-disclosed and consumers know what theyre getting, some might question why government rules stand in the way.

That said, our sense is that additional rules are appropriate when consumers offer prepayment. Experience reveals that prepayments create substantial complexity and risk of dispute: When a consumer offers advance payment in anticipation of service to be provided later, the consumer has little practical recourse if a merchant ultimately falls short. By exploiting consumers overly-optimistic aspirations for when they will redeem their prepayments, sellers can convince consumers to accept short expirations they will systematically fail to redeem in time. And when consumers for whatever reason fail to redeem prepayments, it is less than obvious why the resulting windfall should flow to merchants rather than society as a whole (as escheat laws require). Hence the requirements, separately implemented in so many states, that consumers enjoy additional protections when paying in advance.

A voucher vendor unhappy with applicable legal restrictions has multiple options. The vendor could lobby state legislators to seek modification of laws it considers unwise, unclear, or overly complex. The vendor could restrict its offers to particular states, and it could encourage affected consumers to contact their legislators if theyd like the superior offers available elsewhere. In the interim, the vendor could adjust its offering to comply even with those laws it dislikes. For example, by ceasing to require customer prepayments, a voucher service could avoid restrictions on expiration, cash-back, and abandoned property. Indeed, Restaurant.com sells vouchers at prices often as low as $3, letting customers pay the balance of their (discounted) bill when they dine avoiding most of these complexities described in this article.

In our view, voucher vendors err in ignoring applicable consumer protection law or attempting to disclaim their way out of compliance with legal requirements. With a multi-billion-dollar valuation and more than 7,000 employees, Groupon is particularly well-positioned to review applicable laws. Indeed, NCSL, Texas ABC, and others have already prepared tables of key provisions, easing the necessary research. And if Groupon ultimately finds some laws ambiguous, it could write to applicable regulators to request clarification, just as Edelman contacted tax authorities in Massachusetts.

No doubt some will write off our concerns as trivialities or passing errata. We disagree. For one, we value the principles of consumer protection law, and we hesitate to discard rights consumers have fought for years to obtain. Furthermore, the amounts at issue are substantial: Groupons S-1 anticipates selling $2 billion of vouchers in 2011. An extra 7% tax on that amount would be $140 million taken from consumers, and 15% nonredemption would cost a further $300 million. Finally, we are alarmed by the overall attitude of voucher vendors disparaging the prospect of legal obligations while taking aggressive positions on every question of consumer protection, offering exceptionally narrow visions of their respective responsibilities, and declining to recognize the well-established obligations that accompany their chosen business model. Using these tactics opens voucher vendors to substantial regulatory scrutiny, and in our view that scrutiny is well-deserved.

Posted: June 14, 2011. Updated: June 21, 2011.

Sign

up for notification of major updates and related work.